ETC posts third straight profitable year on defence sim backlog

Environmental Tectonics Corporation (ETCC), the Pennsylvania-based maker of flight simulators, altitude chambers, and disaster-management training systems, has reported net income of $3.0 million for fiscal 2026, marking its third consecutive year of profitability after a period of restructuring. Full-year net sales came in at $62.7 million, broadly flat against the $62.9 million recorded in fiscal 2025, while diluted earnings per share stood at $0.15 compared to $0.75 the prior year.

The headline profit decline, a 76.7% drop in net income, is largely a tax-timing artefact rather than an operational deterioration. Fiscal 2025 benefited from a $5.6 million tax credit following the reversal of a deferred tax asset valuation allowance; the underlying operating picture is steadier, with gross profit margin holding at 28.0% on a reported basis and reaching 33.8% when third-party Aeromedical Centre building revenues are stripped out, up from 32.1% the prior year.

Backlog and bookings point forward

The more strategically relevant number is the order book. Chief Executive Robert Laurent reported a backlog of $61 million at the fiscal year-end of 27 February 2026, and said three contract awards totalling approximately $37 million announced in the first quarter of fiscal 2027 are expected to push the backlog above $80 million. That trajectory, backlog growing faster than annual revenues, suggests ETC is building forward cover at a meaningful rate for a company of its size.

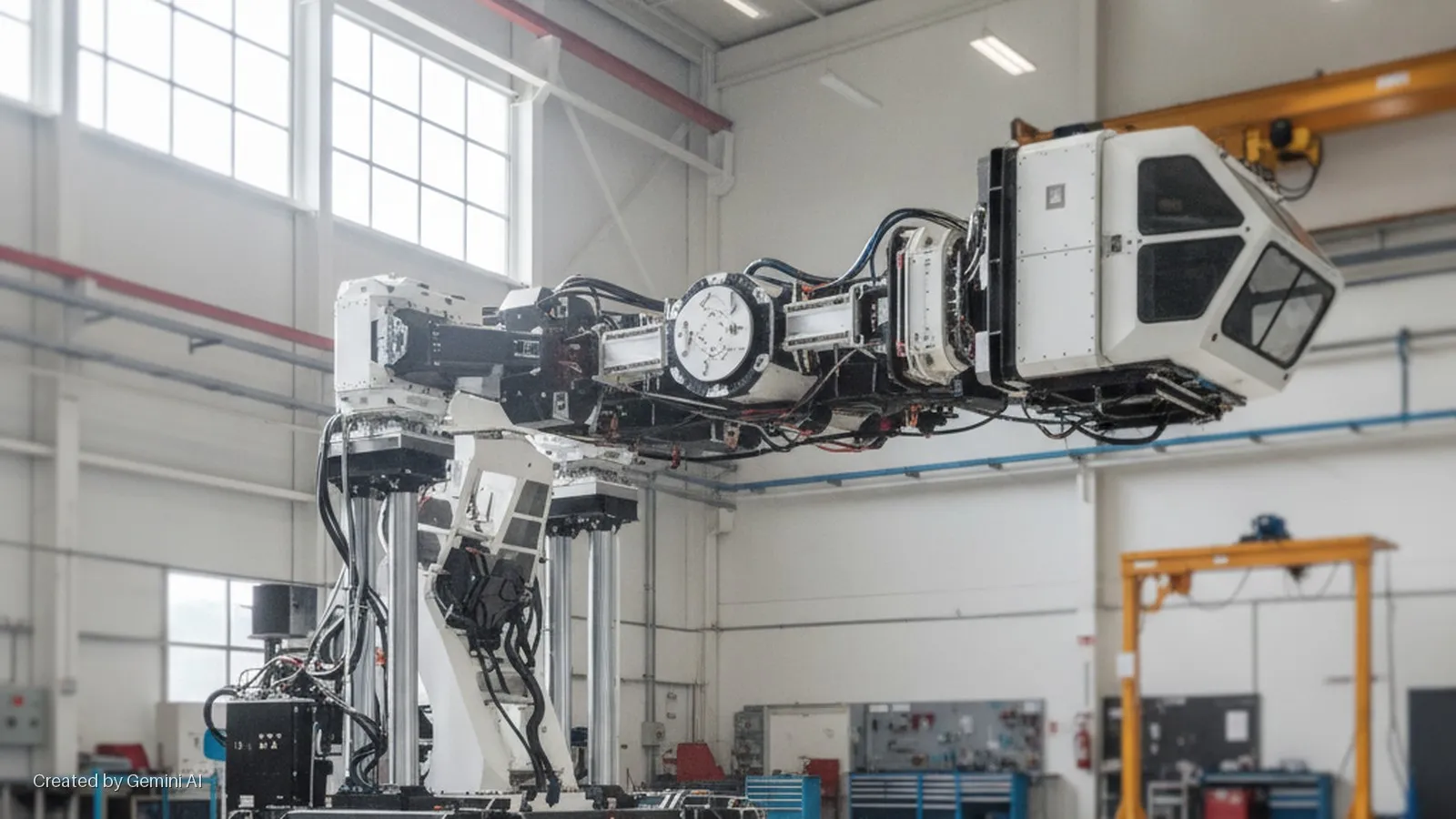

The company operates across two segments. Aerospace Solutions covers aircrew training systems, flight simulation, spatial disorientation trainers, and its Advanced Disaster Management Simulators. Commercial and Industrial Systems covers steriliser units and environmental testing equipment sold into healthcare, pharmaceutical, and automotive markets. The fiscal 2026 softness was concentrated in steriliser sales and the subcontracted Aeromedical Centre build; the core aerospace simulation lines held up, with ETSS and ADMS revenues each growing sharply in Q4 on a sequential and year-on-year basis.

Chief Financial Officer Tim Kennedy highlighted that ETC's PNC credit facilities were extended by two years to June 2028 in May 2026, providing balance-sheet runway. Available liquidity under the revolving credit line was $1.9 million as of mid-June 2026, a modest buffer for a company carrying $12.6 million in drawn borrowings.

The convergence context: defence simulation at a crossroads

ETC's story sits at a quietly important intersection for Disrupts readers. Governments across NATO and the Indo-Pacific are increasing training budgets as real-equipment costs, fighter jets, orbital vehicles, suborbital platforms, make live-hours prohibitively expensive. Simulation and synthetic training environments are absorbing that displaced spend, and the convergence of higher-fidelity AI-driven scenario generation with physical hardware (altitude chambers, centrifuges, motion platforms) is reshaping what a "training system" contract actually looks like.

ETC's product line straddles physical and software-driven simulation, and its Polish subsidiary ETC-PZL adds a European manufacturing dimension that is relevant in a post-2022 NATO procurement environment where friend-shored supply chains carry political as well as logistical value.

For cross-sector investors, ETC remains a micro-cap, roughly $60 million in annual revenues, trading on the OTC market, so it is not a bellwether for the broader defence-simulation sector in the way a prime contractor would be. Nevertheless, its backlog growth is directionally consistent with a wider industry trend: government buyers are locking in longer simulation contracts as budgets rotate away from platform procurement toward readiness and training capability. That shift, if it continues, has compounding implications for adjacent sectors including AI-driven scenario synthesis, cloud-delivered training environments, and the digital-twin infrastructure that underpins next-generation military readiness.

The company's forward guidance is cautious and qualitative, citing anticipated milestone payments on international contracts and expected deposits on fiscal 2027 bookings as the primary liquidity levers for the year ahead.